Buying a car is exciting—but the sticker price is only the beginning. Many buyers focus on monthly payments and forget the true cost of ownership, which can quietly add thousands of dollars per year.

If you’re planning to buy a car, you need to understand what it actually costs to own and operate it, not just to purchase it.

This guide breaks everything down so you can confidently calculate your real vehicle cost before you commit.

Why Most People Misjudge Car Costs

When people budget for a car, they usually think:

- Monthly loan payment

- Gas

- Maybe insurance

But the real cost includes several hidden expenses that often surprise new owners:

- Depreciation (biggest cost most people ignore)

- Insurance changes based on vehicle type

- Maintenance and repairs

- Taxes and registration fees

- Fuel efficiency differences

- Financing interest over time

- Unexpected repairs and wear

In many cases, the true cost of owning a car is 40%–70% higher than the loan payment alone.

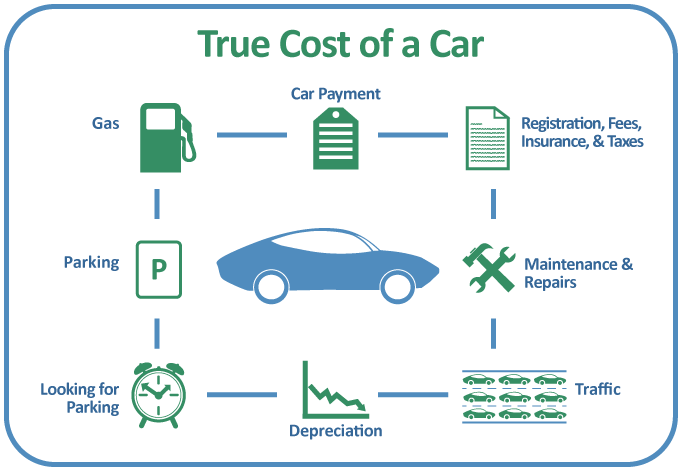

The 6 Key Costs of Vehicle Ownership

To calculate your real cost, break everything into six categories:

1. Depreciation (The Hidden Biggest Cost)

Depreciation is the value your car loses over time. It is often the largest cost of ownership, even more than fuel or insurance.

How it works:

Most vehicles lose:

- 20%–30% in the first year

- 50%+ within 5 years

Example:

If you buy a $30,000 car:

- After 5 years it may be worth $12,000–$15,000

- That means you “lost” $15,000–$18,000 in value

That loss is your real cost.

2. Insurance Costs

Insurance varies widely based on:

- Age

- Driving history

- State

- Vehicle type

- Safety ratings

Sports cars or luxury vehicles can cost 2–3x more to insure than economy cars.

Tip:

Before buying, always check insurance quotes for that exact model—not just averages.

3. Fuel Costs

Fuel is one of the easiest costs to underestimate.

Formula:

- Miles driven per year ÷ MPG × fuel price = annual fuel cost

Example:

- 15,000 miles/year

- 25 MPG vehicle

- $3.50/gallon gas

That’s around:

- $2,100 per year in fuel

If you switch to a 40 MPG car, you could save nearly $1,000 per year.

4. Maintenance and Repairs

Every car requires maintenance:

- Oil changes

- Brake pads

- Tires

- Battery replacement

- Unexpected repairs

Average yearly cost:

- Economy cars: $500–$900

- Mid-range: $800–$1,500

- Luxury vehicles: $1,500–$3,000+

Older cars typically cost more in repairs, even if they’re cheaper upfront.

5. Taxes, Registration & Fees

These vary by location but often include:

- Sales tax (4%–10%+ in many states)

- Annual registration fees

- Title fees

- Emissions testing

Example:

A $25,000 car in a 6% tax state:

- $1,500 in taxes upfront

- Plus annual registration fees

6. Financing Costs (Interest)

If you take a loan, interest adds significantly to the total cost.

Example:

- $25,000 car loan

- 7% interest

- 5-year term

You may pay:

- $4,000–$5,000+ in interest alone

That is money most buyers don’t include in their “car budget.”

Real Example: Total Cost of Ownership

Let’s break down a realistic mid-range vehicle:

Car Price: $30,000

| Cost Category | Annual/Total Cost |

|---|---|

| Depreciation (5 years) | $15,000 |

| Insurance (5 years) | $7,500 |

| Fuel | $10,000 |

| Maintenance | $5,000 |

| Taxes & Fees | $2,000 |

| Loan Interest | $4,500 |

👉 Total Real Cost (5 years):

$44,000–$50,000

That’s far more than the sticker price.

Why This Matters Before You Buy

Understanding total cost helps you:

- Avoid buying a car you can’t truly afford

- Compare vehicles properly (not just price tags)

- Choose fuel-efficient or cheaper-to-insure models

- Reduce long-term financial stress

A slightly more expensive car upfront can actually be cheaper over time.

Smart Ways to Lower Your Car Ownership Cost

Here are practical ways to save money:

1. Choose lower insurance vehicles

Sedans and SUVs with high safety ratings cost less to insure.

2. Prioritize fuel efficiency

Even a 5–10 MPG improvement can save hundreds per year.

3. Avoid unnecessary upgrades

Luxury trims increase depreciation and insurance costs.

4. Buy slightly used instead of new

You avoid the biggest depreciation hit (first 2–3 years).

5. Compare loan rates before buying

Even a 1% difference saves hundreds.

Final Thoughts

A car is not just a purchase—it’s a long-term financial commitment.

Before you buy, always calculate:

- Depreciation

- Insurance

- Fuel

- Maintenance

- Taxes

- Financing

When you combine all six, you’ll see the real picture of ownership—and make a smarter financial decision.

Quick Takeaway

If you remember only one thing:

The true cost of a car is not its price—it’s everything it costs to keep it on the road.